Market Update

Freight Market Update: May 16, 2024

North America vessel dwell times and other updates from the global supply chain | May 17, 2023

Freight Market Update: May 16, 2024

Trends to Watch

[Ocean - FEWB]

- The Red Sea situation continues to be chaotic with vessels rerouting via the Cape of Good Hope, impacting on-time performance and schedule reliability.

- Bookings remain strong after the Chinese Labor Holiday. Another round of GRI (General Rate Increase) for the second half of May is confirmed for $1000 per 40-foot container. Shippers are pushing cargo for earlier departure to avoid further freight cost increase. Unless space has already been secured, all vessels are full. To push cargo on sooner ETD (estimated time of departure) and avoid delays, more carriers are open to Premium options to get cargo loaded on the first available departure date with higher equipment priority.

- Carriers announced more blank sailings coming in June (three from Ocean Alliance as voided and one from MSC as slide-down).

- Carriers are also trying to push for another GRI for the first half of June, considering the current over-demand. Flexport will continue to monitor the market developments.

- More equipment shortages were reported by CMA/Evergreen/Hapag Lloyd/Yangming/HMM. Foreseeing the situation will be tough through May until empty containers are fully recovered. It is highly recommended to pick up containers right after the container yard opens, or as soon as EIR (Equipment Interchange Receipt) is available to print per carrier local practice. Don’t wait till the last minute!

[Air - Global] (Data Source: WorldACD)

- Global Tonnage Decline: Worldwide air cargo tonnages decreased by 12% WoW in the week starting April 29, primarily impacted by China’s Labor Day holiday and Japan's Golden Week, with significant WoW declines in Asia Pacific (-16%) and moderate falls in other regions, including Europe and Central & South America.

- Rate and Demand Variances: Despite overall tonnage declines, demand and rates from the Middle East & South Asia (MESA) to Europe remain high, with average global rates rising slightly by 1% from the previous week to $2.51 per kilogram.

- Public Holiday Impact: The week's tonnage fall was largely due to public holidays like China’s Labor Day, which affected multiple regions including Europe, Asia, and Africa. Adjusting for Japan's Golden Week and post-peak flower shipments, the global decline would moderate from -12% to -9%.

- Regional Rate and Tonnage Trends: Year-on-year analysis shows substantial growth in tonnages and rates, particularly from the MESA region to Europe, with significant rate increases also seen from India and Dubai to Europe, reflecting continued strong demand and regional supply chain disruptions.

Please reach out to your account representative for details on any impacts to your shipments.

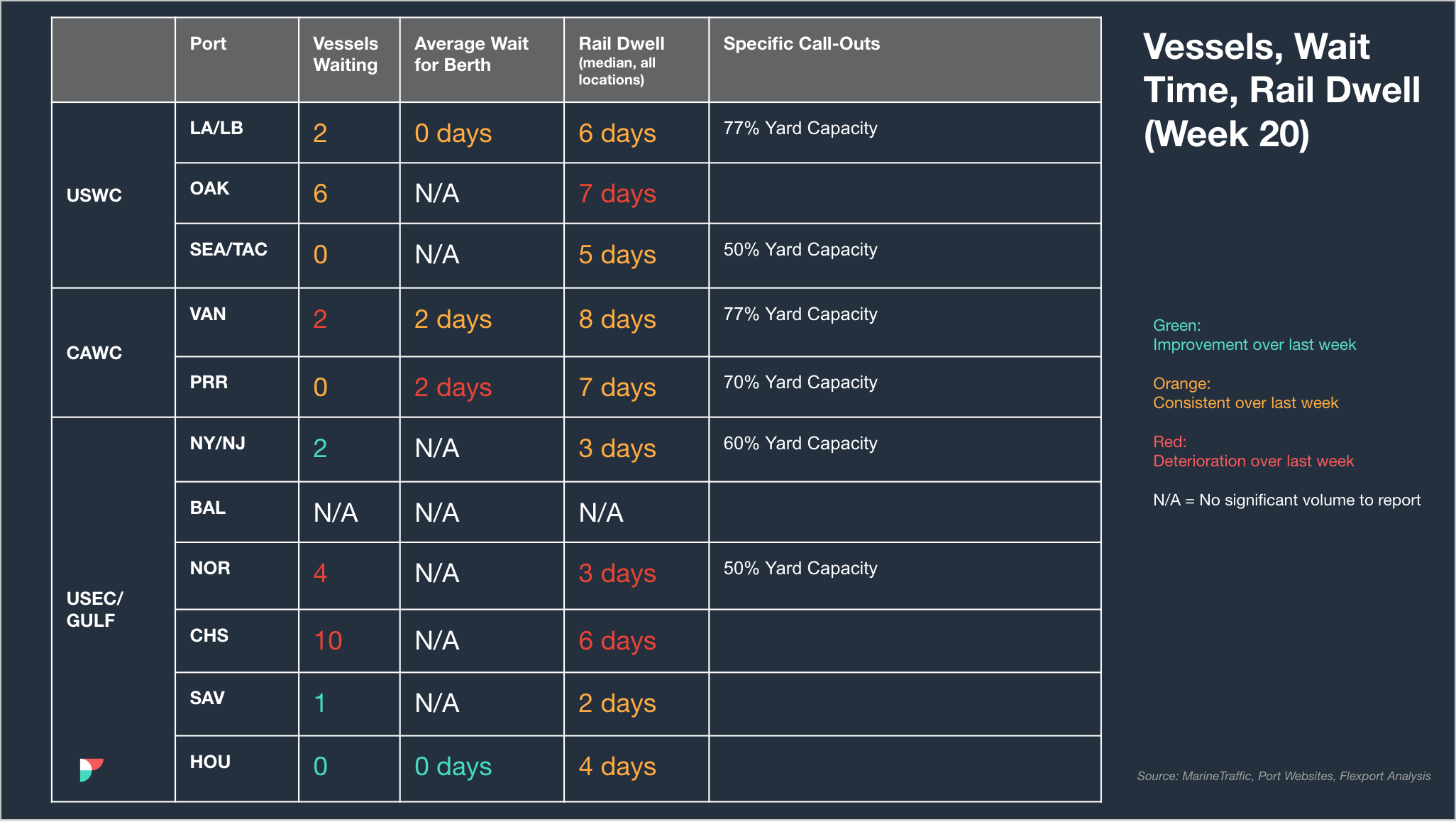

North America Vessel Dwell Times

Webinars

European Freight Market Update Live

Thursday, May 21 @ 16:00 CEST

Scenario Planning: The Political and Economical Impact on Global Supply Chains

Thursday, May 30 @ 17:00 CEST

North America Freight Market Update Live

Thursday, June 13 @ 9:00 am PT / 12:00 pm ET

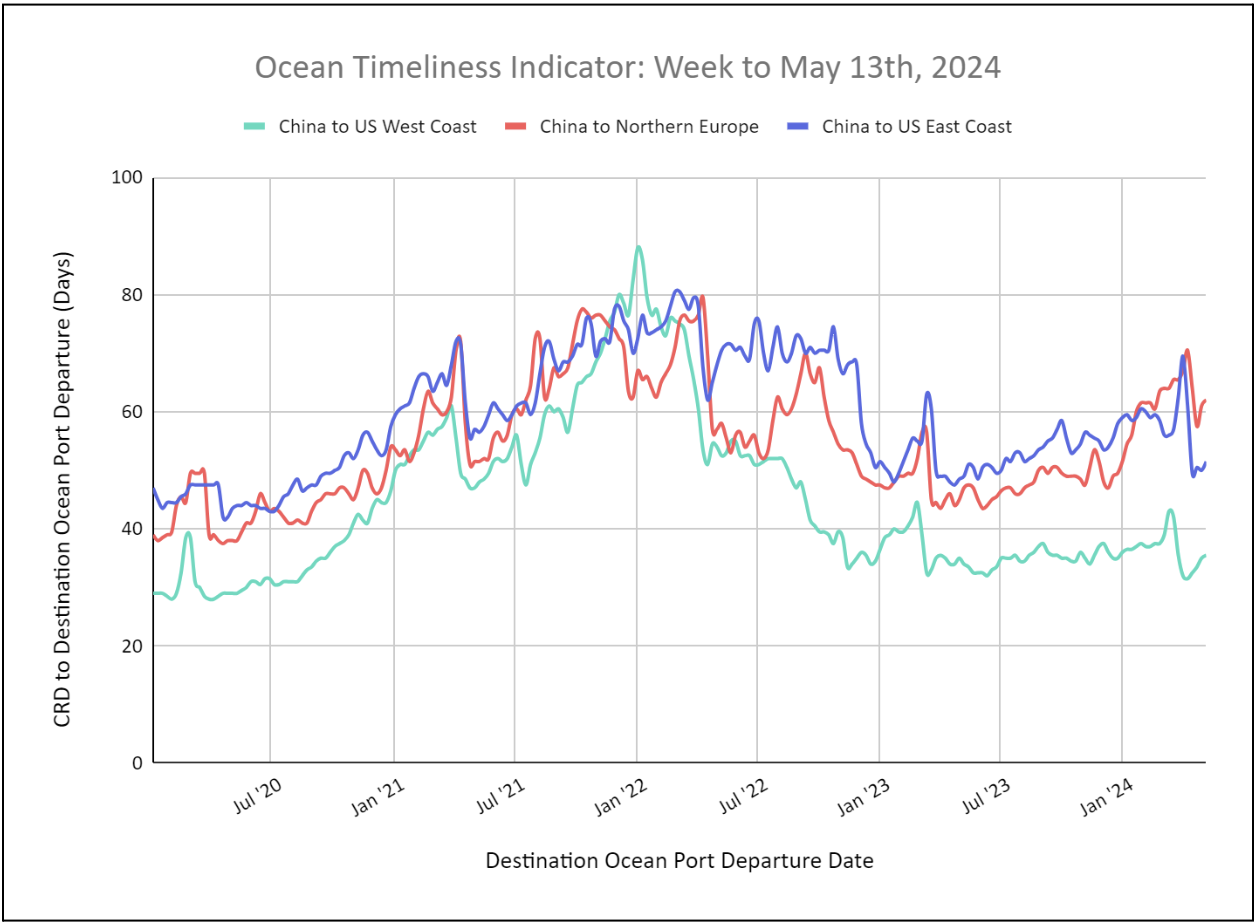

Flexport Ocean Timeliness Indicator

Ocean Timeliness Indicators Increase Across All Major Trade Lanes

Week to May 13, 2024

This week, the OTI for all major trade lanes increased with China to Northern Europe increasing to 62 days due to routing around the Cape of Good Hope, the OTI for China to the U.S. West Coast increasing to 36 days, and the OTI for China to the U.S. East Coast increasing to 52 days.

Please direct questions about the Flexport OTI to press@flexport.com.

See the full report and read about our methodology here.

The contents of this report are made available for informational purposes only. Flexport does not guarantee, represent, or warrant any of the contents of this report because they are based on our current beliefs, expectations, and assumptions, about which there can be no assurance due to various anticipated and unanticipated events that may occur. Neither Flexport nor its advisors or affiliates shall be liable for any losses that arise in any way due to the reliance on the contents contained in this report.

About the Author