Market Update

Freight Market Update: February 22, 2024

North America vessel dwell times and other updates from the global supply chain | May 17, 2023

Freight Market Update: February 22, 2024

Trends to Watch

[Air - Global] (Data Source: WorldACD/Accenture)

- China's Inbound Tonnage Decline: In the week leading up to the Lunar New Year, China experienced a significant drop in inbound air cargo tonnages by 15% week-over-week, contributing to a global tonnage fall of 12%. This was against a backdrop of only a 2% decline in China's outbound tonnages, indicating a sharp contrast in trade dynamics as the holiday approached.

- Stable to Rising Average Global Rates: Despite the drop in tonnages, average global air cargo rates remained steady and even saw a slight increase during week 6, mirroring trends from the previous year. This suggests resilience in pricing amid fluctuating volumes.

- Intra-Asia Pacific Market Slowdown: A notable 17% fall in intra-Asia Pacific traffic largely drove a 3% global tonnage decline, highlighting the region's quick response to the Lunar New Year compared to long-haul markets. Conversely, tonnages from Asia Pacific to certain regions like Central & South America increased, demonstrating varied market reactions.

- Year-on-Year Tonnage and Capacity Increase: Comparatively, weeks 5 and 6 saw a 10% increase in worldwide tonnages year-on-year, with significant rises from Asia Pacific and Middle East & South Asia origins. This was accompanied by a substantial 16% increase in global air cargo capacity, indicating an overall growth in the air cargo sector from last year.

Pricing Trends and Pre-Covid Comparison: Despite a year-on-year drop in average worldwide rates by 14%, the gap is narrowing, and rates remain significantly above pre-Covid levels (34% increase compared to February 2019), suggesting a sustained recovery and adaptation in the air cargo market post-pandemic.

[Ocean - ISC to North America]

- Rates: Increased due to 2H February General Rate Increases (GRIs), but as of week 8 are starting to mitigate. Overall levels still remain significantly inflated compared to November levels at +250% to United States East Coast (USEC) BP and +90% to United States West Coast (USWC) BP.

- Space: Vessels delayed in getting to destination and back to origin are resulting in a lack of capacity. The short-term disruption is expected to be more challenging, while longer term we expect some normalization due to new builds, faster vessel speeds, and implementation of idle capacity.

- Equipment: Although equipment availability is carrier-specific for each port of loading, the overall situation is challenging. This is especially true at inland container depots and smaller/less connected ports.

Please reach out to your account representative for details on any impacts to your shipments.

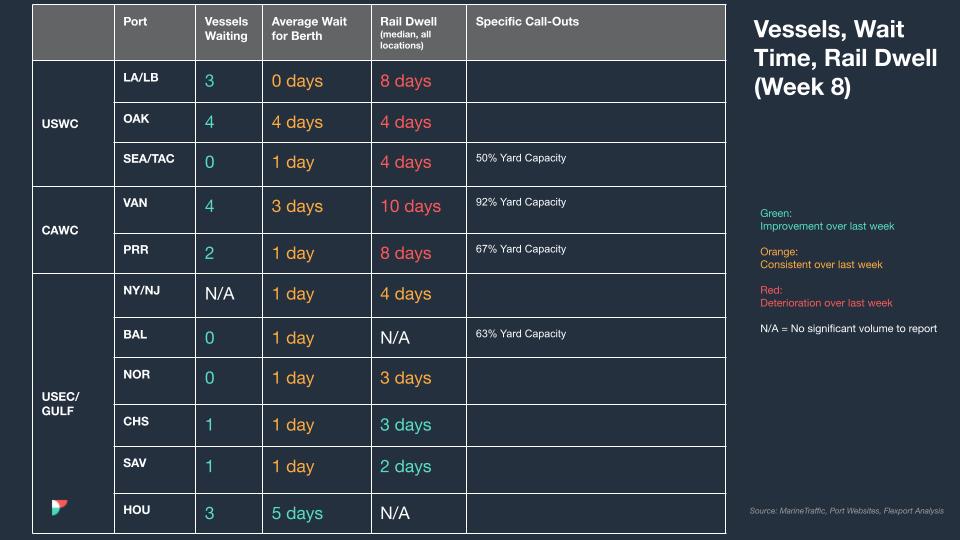

North America Vessel Dwell Times

Webinars

European Freight Market Update Live

Tuesday, March 5 at 15:00 GMT / 16:00 CET

North America Freight Market Update Live Thursday, March 14 at 9:00 AM PT / 12:00 PM ET

[WATCH ON DEMAND] North America Freight Market Update Live

Recorded on Thursday, February 15

This Week In News

Cargo Diversions To West Coast Have Started, LA Port Director Confirms

Shippers are rerouting their cargo to the West Coast of the United States, particularly to the Port of Los Angeles, to avoid security concerns in the Red Sea and drought-related issues at the Panama Canal. Despite not experiencing a surge in freight, the port has observed an increase in cargo volumes, with January marking the second busiest month on record. Retailers are actively replenishing inventories ahead of Lunar New Year closures, and positive economic indicators suggest continued spending by American households.

Import Demand Growth Robust Leading Into Lunar New Year

Bookings for freight bound for the top four U.S. port complexes had surged compared to last year in the lead-up to the Chinese New Year, particularly from China, prompting a notable shift in the supply chain. This spike in orders signifies a departure from the minimal increase seen last year due to pandemic-related inventory surpluses. The rise in demand, especially in Southern California ports, may be influenced by geopolitical conflicts and disruptions like the Red Sea conflict and drought in Panama. Importers are willing to pay higher rates to ensure timely delivery of goods, indicating potential spring demand.

Freight Shipments And Expenditures See January Declines, Notes Cass Freight Index

The January edition of the Cass Freight Index reveals sequential and annual declines in freight shipments and expenditures. Shipments fell 7.6% annually, continuing a trend from previous months, while expenditures dropped 24.3% annually, following a record surge in 2021 and subsequent increases in 2022. Despite harsh winter weather, the decline in shipments aligns with normal seasonality, indicating a potential improvement in freight trends. ACT Research suggests that with destocking and rising goods consumption, the freight downturn may be nearing its end, anticipating improved freight demand fundamentals in 2024.

Rising Inflation Driving Food Supply Chain Robberies

Food theft in the global supply chain has surged, now comprising a third of all hijacking incidents, with a 29% increase in 2023 compared to 2022 levels, according to the British Standards Institution (BSI). This rise is attributed to thieves targeting basic goods experiencing significant price hikes due to inflation. Notably, food and beverage items now represent 22% of overall theft, with agricultural products accounting for 10%. While thefts from facilities have decreased, thefts from containers or trailers have risen sharply. Lack of secure truck parking is cited as a major factor, with road haulage sectors in Europe being particularly vulnerable.

About the Author